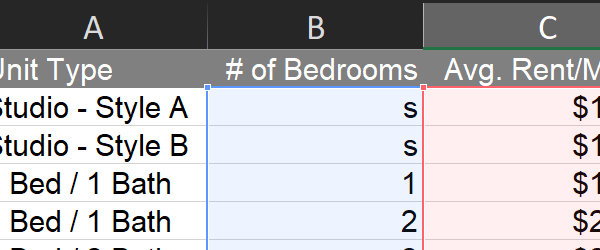

Analyzing apartment unit mixes is a common task for those underwriting multi-family assets. The unit mix summary table reports on individual apartment unit rent roll data on a categorized basis,... read more →

REFAI is officially here! Watch the launch webinar below to learn from Dr. Peter Linneman and Bruce Kirsch how working hard to achieve the REFAI Certification could accelerate your career... read more →

Due to popular demand, we have created a Self Study version of our acclaimed 2-day live training "New York Course", and it's a terrific value for professionals and students. .... read more →

This week marks the fifth anniversary and the 500th blog post of Model for Success. Here's how you can get the most out of the wealth of valuable free information and... read more →

This is an excerpt taken from our Value Add Apartment Building Acquisition tutorial, but applies to all pro forma models across property types. Enjoy. https://www.youtube.com/watch?v=Q4J7rYWxhx4

*** You can get the Excel file by accessing the full free tutorial here. *** In this FREE hands-on-the-keyboard “build it together” Excel tutorial, you will learn how to model... read more →

Real estate expert Peter Linneman, PhD, discusses one way to invest personally in commercial real estate. Get more insights like this through The Real Estate Finance and Investments Certification (REFAI)... read more →

Real estate expert Peter Linneman, PhD, describes the capital stack in commercial real estate. Get more insights like this through The Real Estate Finance and Investments Certification (REFAI) from Linneman... read more →

What do people mean when they say, I'm looking at an A property, or I just sold a B property, or I refuse to invest in a C property? Real... read more →

Real estate expert Peter Linneman, PhD, breaks down LTV, a key term in the real estate jargon lexicon. Get more insights like this through The Real Estate Finance and Investments... read more →

The most common term you'll hear in real estate investment and finance is cap rate. Real estate expert Peter Linneman, PhD, explains. Get more insights like this through The Real... read more →

Real estate expert Peter Linneman, PhD, talks about debt maturity in commercial real estate. Get more insights like this through The Real Estate Finance and Investments Certification (REFAI) from Linneman... read more →

Real estate expert Peter Linneman, PhD, describes NOI, an essential term in the real estate jargon lexicon. Get more insights like this through The Real Estate Finance and Investments Certification... read more →

Real estate expert Peter Linneman, PhD, talks about what all commercial real estate asset types have in common. Get more insights like this through The Real Estate Finance and Investments... read more →

Download the world's best real estate resources directly to your computer. Click here to join the 1,000's of other real estate professionals who have already done so.